L'Autorità Garante della Concorrenza e del Mercato, in data 26 luglio, ha autorizzato con condizioni…

Online intermediaries: impact on the Eu economy

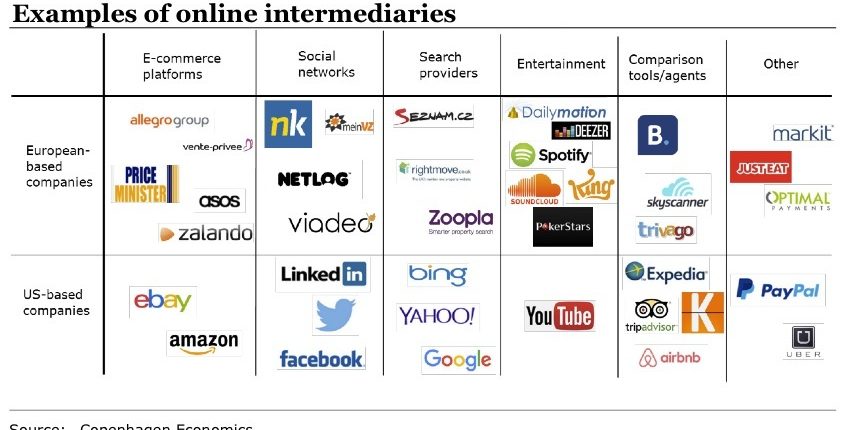

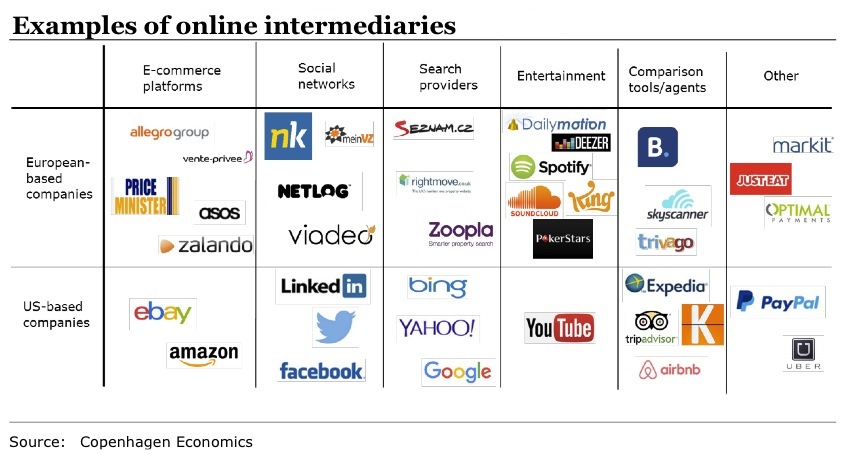

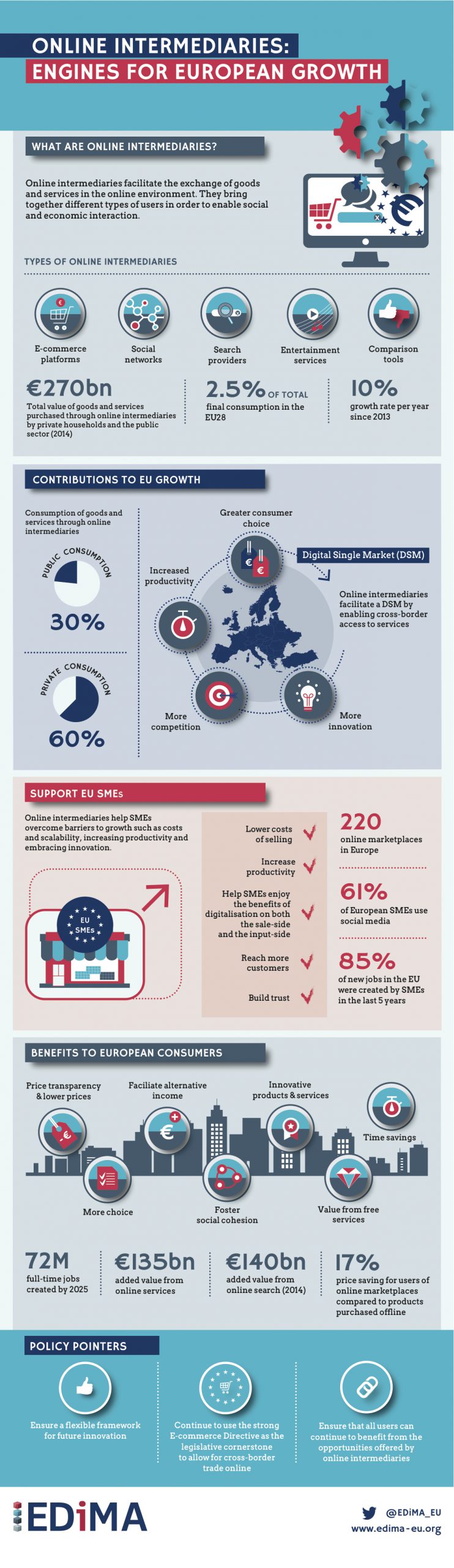

“The Internet as we know it today relies on the efficient operation of online intermediaries. Online intermediaries provide platforms for and facilitate the exchange of goods, services or information in the online environment. They perform or provide activities such as search, e-commerce, social networks and cloud computing. The main feature of online intermediaries (in contrast to other online services) is that online intermediaries bring different types of users together in order to enable economic or social interaction”. It is what we read in the introduction to the study “Online intermediaries: impact on the Eu economy”, commissioned by EDiMA [*] and prepared by Copenhagen Economics. The goal of the study is to contribute to the debate on the future of Europe’s digital economy by assessing the economic contribution of online intermediaries in terms of European growth.

Environment overview – In chapter 1, the study looks at the combined economic size of the online intermediaries in Europe. The paper estimates that the total value of goods and services purchased by private households and the public sector through online intermediaries was about 270 billion Euros in 2014. This amounts to 2.5 per cent of total final consumption in the EU28.

“While it is difficult to delineate the online intermediaries as a distinct group of companies and to estimate the precise size of online intermediaries in Europe, we estimate that online intermediaries have grown at a rate close to 10 per cent per year since our 2013study. The growth of online intermediaries is expected to continue over the coming years. This is not least because of the diffusion of cloud computing and a rapid growth in e-commerce. European e-commerce turnover has been growing steadily over the years with an annual growth of around 15 per cent. This growth is likely to continue in the years to come”.

Online intermediaries are benefitting from a large single market throughout Europe (and indeed globally) and this will allow online intermediaries to bring benefits to individuals and companies from interacting with each other: “As shown, online intermediaries can continue to bring down barriers and burdens that fragment the European online markets and help cross-border e-commerce to grow. The development of a full Digital Single Market is the key enabling policy framework for online intermediaries. In further developing the DSM, it is essential to preserve a flexible regulatory framework governing online intermediaries in the EU and this will underpin the economic growth we see being generated by online intermediaries. Conversely, any adverse changes to the liability regime – such as increased legal obligations on intermediaries – could have a handicapping effect on innovation and the economic activity of online intermediaries, putting this value at risk. As a result, the bar for intervening in the market should be high. The intermediaries’ contributions to the economy would not be possible at the current level without the liability regime as it is currently designed. Preserving and improving the regulatory framework governing online intermediaries in the EU will underpin the economic growth we see being generated by online intermediaries”.

Contributions to EU SMEs – In chapter 2, the study looks at how online intermediaries help Europe’s small and medium-sized enterprises (SMEs) to grow. SMEs are the backbone of Europe’s economy: SMEs have created around 85 per cent of the new jobs in the EU in the last five years and now account for two-thirds of the total private sector employment. However, Europe’s SMEs face various barriers to growth, in particular when entering new markets.

“Importantly, online intermediaries help European SMEs overcome these barriers by making it easier to enter a market and reach consumers. Online intermediaries help smaller companies achieve big company benefits from digitalisation. Online intermediaries allow smaller companies to become early adopters of the new Internet technologies and business models. Furthermore, online intermediaries allow SMEs to enjoy these benefits at a fraction of the cost that they would incur without them”.

“The results – says EdiMa – speak for themselves. SMEs that are early adopters of advanced information technologies have created jobs twice as fast and grown revenue faster than SMEs with a slower adoption rate. Research based on European data shows that online marketplaces reduce the trade costs for SMEs. As a result, more SMEs can engage in exporting. Online intermediaries also allow each SME to serve more export markets. Another recent EU study examines the impact of a well-functioning liability regime for Internet intermediary start-ups and found significant impact on the viability and success of start-ups. The chapter further provides real life examples of SMEs that benefit from online intermediaries”.

SMEs most notably benefit are summarizedby EdiMa in three key aspects:

- Lower costs of selling: online intermediaries facilitate low cost selling, which means that the amount of capital required to start and grow a business is reduced.

- Reaching more customers: online intermediaries enable SMEs to reach more potential buyers, which reduces the need for new capital investments and resources required to grow to scale.

- Building trust: online intermediaries help SMEs to build a trusting relationship with their customers.

“Overall, we find that online intermediaries reduce important barriers to the growth of SMEs. It is therefore important to the growth of Europe’s SMEs to provide online intermediaries with a policy framework flexible enough to allow them to continue to help SMEs to grow. With regards to sales, SMEs use social networks, recommendation engines, and search engines to reach new customers. Merchant platforms such as Allegro, eBay and Etsy help SMEs to market their products and it helps SMEs to become exporters and go beyond borders. Payment facilitators such as PayPal, PayU, Wikipay and Square provide access to credit provision and payment systems. Logistics platforms link SMEs to a global network of shipping companies”.

With regards to input, “SMEs use peer-to-peer business platforms (sharing economy) such as 3Dhubs.com or Floow2 to get capacity online of everything from 3D printers, specialised machinery, tools to secretary assistance. SMEs use online workforce marketplaces such upwork.com as a platform to hire and work with independent professionals around the world. Cloud computing has enabled SMEs to enjoy hardware and software benefits once limited to bigger companies. Platforms such as Funding Circle link those SMEs who need capital to interested investors”.

Consumers – “Online intermediaries – says EdiMa – also unlock benefits for consumers. Firstly, online intermediaries benefit consumers through the traditional channels in standard consumer theory such as more price transparency, more choice and time savings. Some of these effects are a mirror image of the effects on SMEs. For example, by bringing down barriers to entry and growth for SMEs, online intermediaries provide consumers with more choice and, in particular, more niche products, which benefit consumers. Online intermediaries allow consumers to access an enormous amount of information very quickly and locate sellers beyond those companies that are locally accessible. In addition, online intermediaries can work as a source of income for individuals, as they can offer their own products or services to other users quicker than ever before. Lastly, online intermediaries affect people not only as consumers but also as citizens whose utility and well-being depend on factors beyond those that can be captured by standard economic measures. For example, online intermediaries can help support important society goals such as democracy or freedom of speech and can enable social capital formation. These effects are all part of online intermediaries’ broader impact on EU consumers”.

It is difficult to quantify all of these benefits, especially those that go beyond traditional economic measures. EdiMa presents quantifications of specific examples of some of the benefits: “In particular, we show that online marketplaces enable lower prices to a total value of 1 billion Euros while an increased availability of niche books result in benefits of 4-5 billion Euros for European consumers. Free social networking services, wikis, generalised search services and comparison shopping generate a consumer surplus of 22 billion Euros. Lastly, we show that online search platforms generate time savings worth 140 billion Euros for European consumers. Finally, we discuss the policy environment in which online intermediaries operate. We furthermore validate that the liability regime set out in the EU e-commerce Directive is an important factor supporting the role online intermediaries are playing and the activities they are enabling. Indeed, the online intermediaries’ contributions to the economy would not be possible at the current level without the liability regime as it is currently designed”.

“When assessing the role of online intermediaries in the economy and the appropriate policy framework, we therefore argue that it is essential to preserve the limited liability regime governing online intermediaries in the EU in order to underpin the economic growth generated by online intermediaries and to strengthen their facilitating abilities to support the European economy. Conversely, any adverse changes to the liability regime – such as increased legal obligations on online intermediaries – could have a handicapping effect on innovation and the activity of online intermediaries, putting this value at risk, and based on the analysis in this report, we would strongly recommend not to re-open the e-commerce Directive or impose new monitoring requirements on online intermediaries”.

European online intermediaries are already regulated in many ways through numerous EU directives and regulations. A regulatory mapping of the Regulations and Directives applicable to online intermediaries identified more than 40 EU Directives and Regulations covering many different aspects of the activities conducted by online intermediaries ranging from consumer rights to data retention and many more aspects.

“Already today online intermediaries are not operating in a regulatory void and are subject to a large number of regulations of covering all aspects of their activities. Some European policy makers are now considering additional regulation of online intermediaries. The European Commission has decided to launch a comprehensive assessment into the role of online intermediaries in the economy”.

EdiMA indicates three main questions for consideration before additional regulation in the market for online intermediaries should be considered:

- Firstly, it is widely accepted that regulatory intervention of this kind should only be considered where there is clear risk of a serious loss of economic efficiency and consumer welfare; where other solutions are not available; and where it is clear that the regulatory intervention itself, with the distortions that it can create, will not make the situation worse than it would otherwise be.

- Secondly, it is inherently difficult to define the online intermediaries as a special class of companies, and they continue to evolve and change in a variety of ways. Thus attempting to create legislation to cover this practically undefinable class of companies would be extremely challenging.

- Thirdly and finally, the online intermediaries are still young companies and competition in the market is very dynamic. There is intense rivalry between the large online intermediaries and rivalry with a number of other more specialised platforms for the attention of users. As shown in this report, online intermediaries are creating value and online intermediaries continue to innovate at high speed.

[*] EDiMA is the European trade association representing online platforms. It is an alliance of new media and Internet companies whose members include Airbnb, Allegro Group, Amazon EU, Apple, eBay, Expedia, Facebook, Google, King, LinkedIn, Microsoft, Netflix, PayPal, Twitter, Yahoo! Europe, Yelp. 30 novembre 2015

[*] EDiMA is the European trade association representing online platforms. It is an alliance of new media and Internet companies whose members include Airbnb, Allegro Group, Amazon EU, Apple, eBay, Expedia, Facebook, Google, King, LinkedIn, Microsoft, Netflix, PayPal, Twitter, Yahoo! Europe, Yelp. 30 novembre 2015